Breaking the Mold: How Bank Statement Loans Work in San Diego’s Competitive Real Estate Market

San Diego. The name itself evokes images of sun-drenched beaches, a vibrant culture, and a lifestyle that’s the envy of the nation. But for aspiring homeowners, it also brings to mind a real estate market that’s as competitive as it is beautiful. In a landscape of rapid sales and rising prices, securing financing is the critical first step. For many, however, the traditional mortgage process feels like trying to fit a square peg into a round hole. This is especially true for the backbone of San Diego's dynamic economy: the entrepreneurs, freelancers, small business owners, and gig economy workers. If your income doesn't come from a neat and tidy W-2, you've likely felt the frustration. But what if there was a lending solution designed specifically for you? A tool that looks at your actual cash flow, not just your tax returns? Welcome to the world of bank statement loans—a game-changer for buying property in San Diego.

The San Diego Real Estate Conundrum: A Market for the Agile

To understand the power of bank statement loans, we first need to appreciate the unique challenges of the San Diego market. It's not just about high demand; it's about the very nature of our local economy. From the biotech hubs in La Jolla to the thriving tourism sector downtown and the countless independent contractors that keep the city running, San Diego is a city of innovators and self-starters. This economic diversity means a significant portion of the population has non-traditional income streams. While this entrepreneurial spirit drives our city forward, it often clashes with the rigid documentation requirements of conventional lenders.

Traditional mortgages, known as Qualified Mortgages (QM), are built around the W-2 employee. Lenders want to see two years of steady employment, pay stubs, and tax returns that show a consistent, predictable salary. For a business owner who strategically reinvests profits or a freelancer with fluctuating monthly income, tax returns may not accurately reflect their true financial capacity to afford a home. This is the gap that bank statement loans are designed to fill.

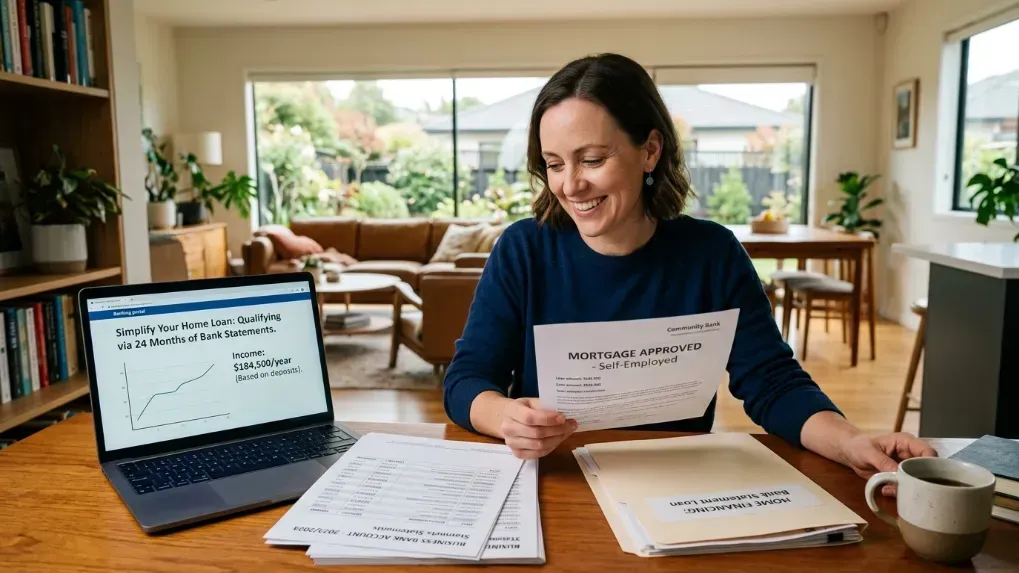

What Exactly is a Bank Statement Loan?

A bank statement loan is a type of Non-Qualified Mortgage (Non-QM) that allows borrowers to use their personal or business bank statements to prove their income, instead of relying on traditional tax documents. Lenders, like our team here at HWH San Diego Hard Money Lender - Real Estate, analyze 12 to 24 months of bank deposits to determine a consistent and reliable monthly income figure. This approach provides a more realistic picture of a self-employed individual's cash flow.

Think of it as showing, not just telling. Instead of showing a tax return that reflects numerous deductions and business expenses, you're showing the actual, consistent flow of money into your accounts. This method acknowledges that taxable income and actual cash flow can be two very different things for a business owner.

Traditional vs. Bank Statement Loans: A Quick Comparison

| Feature | Traditional Loan (QM) | Bank Statement Loan (Non-QM) |

|---|---|---|

| Income Verification | W-2s, tax returns, pay stubs | 12-24 months of personal or business bank statements |

| Ideal Borrower | Salaried employees with consistent paychecks | Self-employed, business owners, freelancers, investors |

| Regulatory Category | Qualified Mortgage (meets strict federal guidelines) | Non-Qualified Mortgage (offers more flexibility) |

| Down Payment | Can be as low as 3-5% | Typically requires 10-20% or more |

| Interest Rates | Generally lower due to lower perceived risk | Generally higher to compensate for underwriting flexibility |

Who is the Ideal Candidate for a Bank Statement Loan in San Diego?

This powerful financial tool is tailored for a specific type of buyer. You might be a perfect fit if you fall into one of these categories:

- Small Business Owners: Restaurant owners in the Gaslamp, boutique shopkeepers in North Park, or construction contractors in East County who have significant revenue but also significant business write-offs on their taxes.

- Self-Employed Professionals: Independent real estate agents, financial consultants, attorneys, and marketing gurus who operate as sole proprietors or LLCs.

- Freelancers and Gig Economy Workers: The graphic designers, writers, Uber drivers, and software developers who make up a growing part of San Diego's workforce. Their income may be project-based and fluctuate month-to-month, but their bank statements show a strong annual average.

- Real Estate Investors: Individuals who own multiple properties and have complex income streams from rent and other investments that don't fit neatly into a traditional lender's box.

- Seasonal Workers: Professionals in industries like tourism or events whose income is concentrated in certain parts of the year but is substantial overall.

The Nitty-Gritty: How Lenders Qualify You

Securing a bank statement loan is a detailed process, but it’s straightforward when you know what to expect. Here’s a breakdown of how lenders typically assess your application:

- Document Collection: This is the most crucial step. You'll need to provide complete, consecutive bank statements for the required period, usually 12 or 24 months. You'll need every single page. Some lenders may also ask for a Profit & Loss (P&L) statement prepared by you or a CPA, and a letter from your accountant verifying your self-employment status.

- Income Calculation: This is where the magic happens. The lender’s underwriter will meticulously analyze your deposits.

- For Business Accounts: They will total all business-related deposits and then apply an “expense factor” (typically between 30-50%, depending on the industry) to arrive at a qualifying income. For example, if your business deposits average $30,000 per month and the lender uses a 50% expense factor, your qualifying monthly income would be $15,000.

- For Personal Accounts: If you use a personal account for business, lenders will often consider 100% of the deposits as income, provided they can clearly identify them as business-related.

- Credit Score and Down Payment: While income verification is flexible, other requirements are still stringent. Most bank statement loan programs require a good to excellent credit score (often 680 or higher). Furthermore, because these are considered slightly riskier loans, a larger down payment is almost always required—typically at least 10-20% of the purchase price. Having significant assets or reserves can also greatly strengthen your application.

- Debt-to-Income (DTI) Ratio: Once your qualifying monthly income is established, the lender will calculate your DTI by comparing that income to your total monthly debt obligations (including the proposed new mortgage payment). Lenders have specific DTI thresholds you'll need to meet.

Weighing the Pros and Cons in the San Diego Market

Like any financial product, bank statement loans come with their own set of advantages and disadvantages. It's important to weigh them carefully.

The Advantages:

- Access to Homeownership: This is the biggest pro. It opens the door to the San Diego property market for a huge segment of qualified buyers who were previously shut out.

- Based on Real Cash Flow: It provides a more accurate assessment of your ability to pay a mortgage than tax returns, which are designed to minimize tax liability.

- Flexibility for Complex Finances: It accommodates variable income, multiple income streams, and the financial realities of running a business.

- Empowers Entrepreneurs: It allows business owners to continue making smart tax decisions without jeopardizing their ability to secure a home loan.

The Considerations:

- Higher Interest Rates: The flexibility comes at a cost. Interest rates on bank statement loans are typically higher than on conventional loans to offset the lender's increased risk.

- Larger Down Payment: You will need more cash upfront. The 10-20%+ down payment requirement can be a barrier for some.

- Meticulous Record-Keeping is a Must: You need to have clean, well-organized bank statements. Large, unexplained cash deposits can raise red flags and delay your application.

- Not All Lenders Are Equal: You need a specialist. Many traditional banks don't offer these types of loans, so working with an experienced lender is key.

Finding the Right Lending Partner in San Diego

The success of your bank statement loan application heavily depends on the expertise of your lender. You need a partner who not only offers these products but also deeply understands the nuances of the San Diego economy and the financial lives of self-employed individuals. A local lender will have a better grasp of property values and market trends from Carlsbad to Chula Vista.

At HWH San Diego Hard Money Lender - Real Estate, we pride ourselves on being that partner. Our team has extensive experience working with San Diego's entrepreneurs and business owners. We believe your hard work and success should be recognized, and we have the tools to make your homeownership goals a reality. To learn more about our approach, you can read about us and our commitment to the local community.

Conclusion: Your Path to a San Diego Home

In San Diego’s competitive real estate market, you need every advantage you can get. For the self-employed, the freelancer, and the business owner, the bank statement loan isn't just an alternative; it's a lifeline. It’s a modern solution for the modern workforce, acknowledging that a successful career doesn't always come with a W-2. By understanding your real cash flow, these loans break down the barriers that have kept so many deserving buyers on the sidelines.

Don't let non-traditional income documentation stand between you and your dream home. If you're ready to explore how a bank statement loan can work for you, the first step is to speak with an expert. Contact our team today, and let's build a strategy to turn your San Diego real estate aspirations into a reality.

Frequently Asked Questions

Can I get a bank statement loan with a poor credit score?

It is challenging. Most lenders offering bank statement loans require a minimum credit score, often in the mid-to-high 600s (with 680+ being a common benchmark). Because the income verification method is non-traditional, lenders rely more heavily on other factors like credit history and a substantial down payment to mitigate their risk.

Are the interest rates for bank statement loans significantly higher than conventional loans?

Yes, you can generally expect a higher interest rate. Rates for Non-QM loans like these are typically 0.5% to 2% higher than for a comparable conventional loan. This premium compensates the lender for the additional flexibility in underwriting and the perceived higher risk associated with non-standard income documentation.

Do I need to provide both personal and business bank statements?

It depends on how you run your business. If you primarily use a business account for all your revenue, you will provide those statements. If you operate as a sole proprietor and use a personal account for business deposits, you will use that. The key is to provide the statements for the account(s) that most accurately and completely show your business-related income. Be prepared to explain the nature of deposits to your lender.

How long does the approval process take for a bank statement loan in San Diego?

The timeline can be very similar to a traditional loan, typically 30-45 days from application to closing. The most time-consuming part is often the upfront analysis of the bank statements. To speed up the process, ensure you provide complete, consecutive statements for the entire required period (e.g., 24 months) with all pages included right from the start.